So, it’s been a while. To be honest, I needed a break – I went on vacation, saw some beautiful places, ate a bunch of delicious food and got a ton of steps hiking around the coast. But now I’m back and staring at the pitiful inventory and it’s time for an update.

Theme of the month: Sellers holding back, some buyers returning, bifurcating the North/East and South/West housing markets.

Media

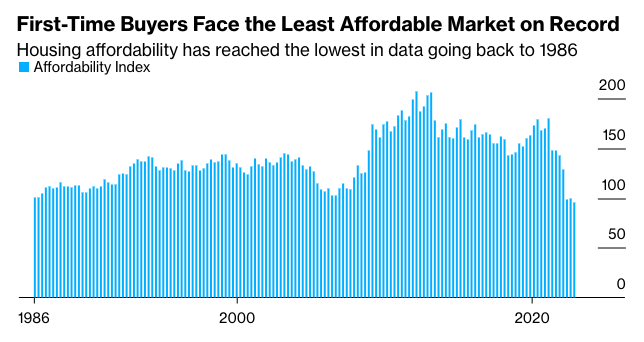

Americans Need to Be Richer Than Ever to Buy Their First Home

The crunch continues as new supply fails to come to market. More and more sellers are sitting on homes or deciding to rent them out to hold on to the pandemic induced rates.

At the same time, rising rates have pushed payments to the “most unaffordable levels in records going back almost four decades“, says Bloomberg.

They make no predictions about home prices in the future but note that parental help is turning out to be a key factor in purchasing a house. The percentage of people using parental help in the form of a down payment or co-borrower has risen in the wake of the pandemic.

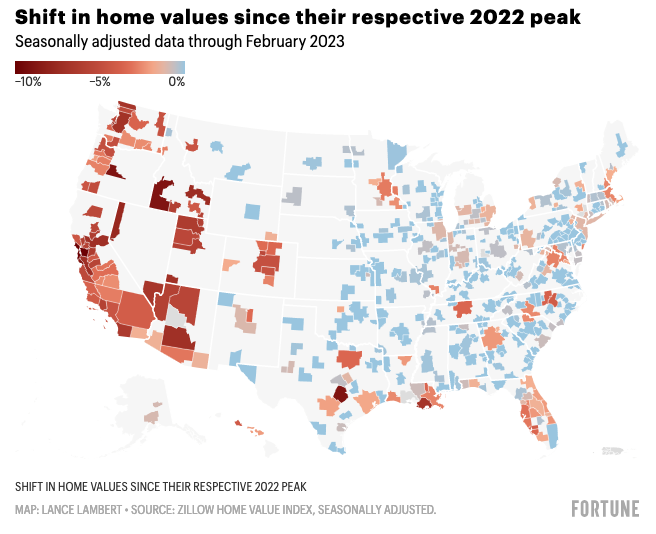

The home price correction is losing steam — geographically speaking

Fortune notes that the market is bifurcating, with some markets regaining steam and others falling behind. A few months ago, 79% of the nation’s 200 largest housing markets saw a month-over-month home price decline. Today that number is 38%.

The difference is geographic. Western and Southern markets continue to decline while MidWestern and North-Eastern markets rise.

Thankfully here in San Diego, we are as western and southern as it gets.

RE Industry

Why bank failures can’t shake the housing market

Realtor.com, brimming with optimism, shares their thoughts on why the banking failures of the past week can’t touch the housing market. If you’ve been under a rock, in the past week several bank failures have shaken confidence in financial markets – SVB, Signature and Credit Suisse have all been taken over by regulators as other banks, like First Republic, continue to teeter.

So, back to Danielle Hale at Realtor.com, “Homes are sitting on the market longer than last year, but the gap isn’t growing”. This suggests that listings may eventually start getting snapped up faster this spring, with Hale saying, “The usual seasonal pick-up in housing market pace is happening.”

SVB Response May Bring Down Mortgage Rates and Chill Tech-Dominated Housing Markets

Zillow is only slightly less optimistic about the results of the bank failures. While they believe that lower mortgage rates will boost the housing market (and so far, that’s been true) they do suggest that tech-dominated markets may be cooled down by the broader market conditions.

Lower rates would help home buyers who are stretched thin when it comes to affordability, but if SVB’s troubles are indicative of wider issues, …

– Zillow

A widespread tech downturn might be felt in housing markets like the San Francisco Bay Area and Seattle, where tech employment and stock prices have an outsized effect.

Pending Home Sales Improved for Second Straight Month, Up 8.1% in January

NAR has been rather quiet, their last post shares that pending home sales have improved for a second month, in January. Of course this is 24.1% less than the year prior but “up 8.1%” sounds better. That said, despite their recent silence, the spring buying season has heated up the market somewhat. It’s hard to gauge exactly how much without more data however.

For the future, NAR anticipates the 30-year fixed mortgage rate steadily dropping to an average of 6.1% in 2023. We have a ways to go from here but it has stayed pretty steadily above 6.5% since this comment. The bank failures may be changing that soon.

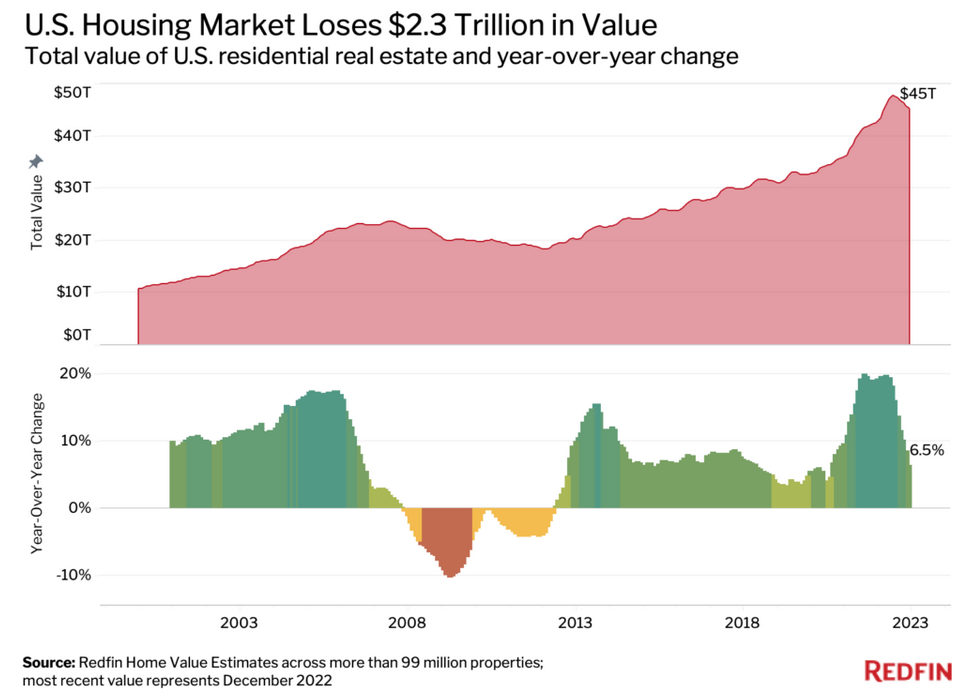

U.S. Homeowners Have Lost $2.3 Trillion in Value Since June Peak

Redfin is decidely gloomy with this headline. The US housing market was worth $47.7 trillion in June and dropped to $45.3 trillion at the end of 2022. They note that the Bay Area has seen the biggest drop in values, with SF, Oakland and San Jose falling the most.

You can see that the drop in the value (red chart) is a pretty small drop. But that slope is nothing to sniff at either – it’s quite a dropoff, even when compared to 2008.

Anecdata

“Scared? No. Cautious? Yes. …With that said, I’m waiting another year and will reassess while I continue to save funds. My rent is lower than a mortgage would be at these prices and interest rates. – First time homebuyer cautious with the possibility of recession.

My brother became rich quick as a real estate agent and it got me rethinking my life goals… While I am a first year law student quickly going into some debt, he just made 500k while being only 24 – Young lawyer rethinking his career choice.

It listed at 399k, I waited and watched it drop to 389k, then 379k. I put in an offer at 375k and we settled at 377k. 6 months ago this house would have likely sold above their initial ask price. – Jacksonville, FL buyer seeing a cooling market.

It was cooling down last fall, but now it’s heating up again because supply has collapsed. My market (Orange County) normally has 3,000 houses listed in February, but this February there were only 1,800. Not many people can afford to buy, but even fewer people want to sell. Thus the “hot” market. – Orange county, CA buyer seeing a hotter market than last fall.

We’re already in 2021 territory. When pulling comps I’m finding 2021 levels for current value in many cases. It’s never across the board though. – Sacramento appraiser Ryan Lundquist on local data.

Disclaimer: I’m an idiot first time home buyer. I’ve never taken an econ class in my life. I’m just sharing what I see and learn as it happens. I am 100% certain I will get things wrong, so don’t take any of this as the golden truth.