I keep seeing people say that this time, it’s different and that just makes me wonder if they were around last time. By last time, I mean the 2008 housing bubble. By this time, I mean the 2022 housing bubble.

The general consensus seems to be that in 2008, a bunch of stupid people took on loans they could not afford and then foreclosed. All of these people were basically unemployed layabouts who decided to take on on NINJA loans – no income, no job, no assets – and lenders gave them the loans without checking anything.

But I was there. My smart, capable coworkers in software engineering also got homes they thought they could afford. They found realtors and lenders and inspectors and trusted them, did what they were told and bought their first houses. This was post dotcom bust, tech employees were not rolling in it but we were doing okay. I was probably making 70k at the time. These coworkers also lost homes in that crash.

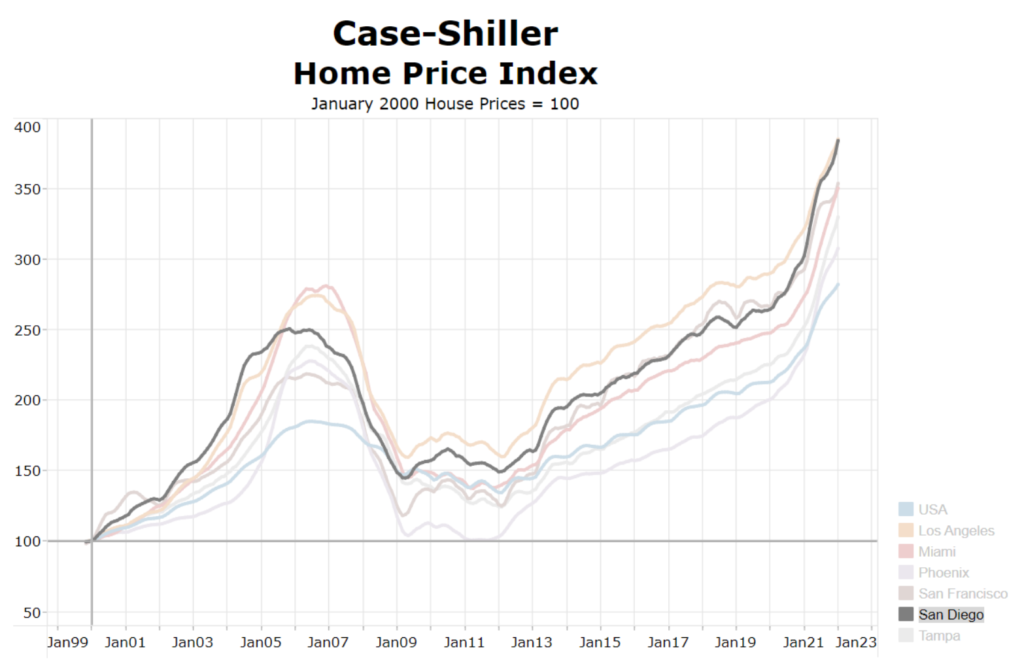

Even today, I hear people say, “Oh, san diego home prices will never go down”. I even sorta believed it, until I looked at the Case-Shiller home price index for San Diego and what really happened in 2006.

People who bought close to the peak between 05-07 were underwater until 2018. That’s a decade of possibly not being able to sell, not being able to refinance, not being able to make other life choices, like a new city, or a job with less pay. Luckily, I didn’t buy and I was saved from being trapped underwater for a decade.

A comparison to 2006

Truth be told, I wasn’t paying a ton of attention to real estate at the time, but recently I stumbled on this blog post from then, talking about the Socal Housing Bubble. This blogger posted this in September 2006 so rather early I would say. I think it’s an incredible look back at the prevailing “wisdom” at that time. It is absolutely worth a read.

While reading it, I was mentally comparing it to the situation today. So I figured why not share that comparison? The following are the reasons the blogger provided for a possible upcoming crash.

1. Speculative Demand

Too much speculative demand for real estate:

Of course there was high demand for a 20% appreciating asset! That’s why there were bidding wars and “please pick me” letters and why houses would sell in one weekend above the asking price.

– WhatBubble

Word for word, this is what we see today. This is absolutely the norm right now – houses selling in one weekend, above asking price, with bidding wars. I’m not sure first time home buyers even realize that that norm used to be 30-40 DAYS ON MARKET. A new trick is waiving all contingencies, appraisal, loan and inspection, which perhaps wasn’t a thing back then.

… even people buying as a “primary residence” knew that the market was so hot, they would be making more money (in their sleep) off of their house (read: investment) than with their 9-5! “You couldn’t lose”!

This point ties in nicely with a recent headline from WSJ that Homes Earned More for Owners Than Their Jobs Last Year. Yes, people are looking at sky high appreciation and the effect of that is accelerated since they can check their Zestimates 5 times a day on their phones. After this crisis is over, we’ll see papers about the effect of Zillow on the post-covid housing market exuberance.

2. Cheap Money

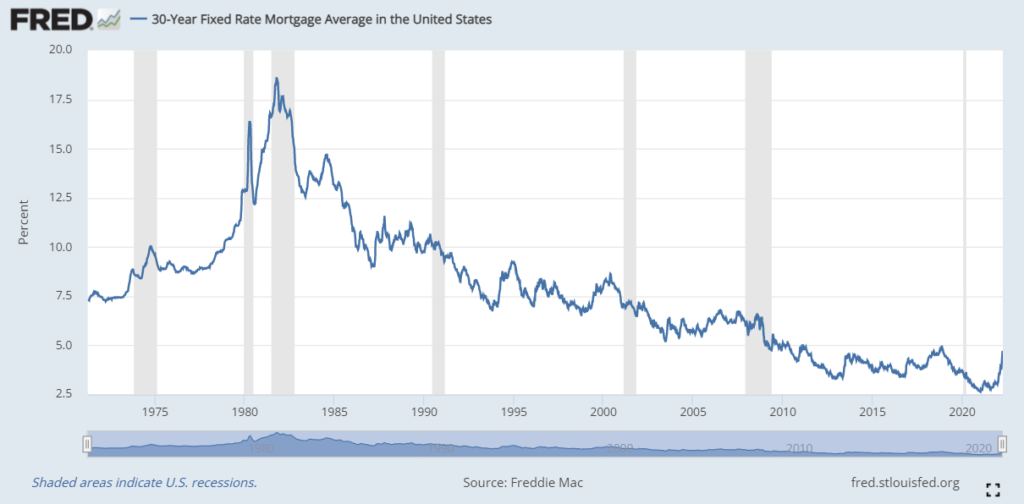

Cheap money. All-time low interest rates made monthly payments low enough that buying a house came into reach for a lot of people even as home prices shot up…

– WhatBubble

In the past two years, we had rates never seen before. In Jan 2021, rates sank to their lowest level in history at 2.65%. If that isn’t cheap money, I don’t know what is. In 2006, we were also at all-time lows but that was still up above 5%.

This cheap money makes homes seem more affordable, which in turn makes the median price go up. Warren Buffett used an excellent analogy when he described interest rates as “financial gravity.”

“Interest rates are like gravity in valuations. If interest rates are nothing, values can be almost infinite. If interest rates are extremely high, that’s a huge gravitational pull on values.”

– Warren Buffett

3. Toxic loans raised the ceiling of affordability

This is the one that everyone points to as proof that this time is different. People took toxic “subprime” loans then, and that isn’t happening now.

These loans can work to a buyers advantage in an appreciating market, but in a depreciating market things get ugly quickly. As stated earlier, a lot of people speculated that prices would continue to rise, accepting the risk of these loans. Other “less sophisticated” buyers were tricked into thinking they could afford these loans by predatory lenders and realtors.

– WhatBubble

The first type of people he mentions, were people who accepted the risk of these loans knowingly, speculating that the house price would rise. The average homebuyer is unlikely to get a very specialized or unique loan today, this is true. But, there are thousands of real estate investors who take risky loans to build their portfolios.

A popular website called BiggerPockets promotes a method called BRRRR – Buy, Rehab, Rent, Refinance, Repeat. An FT article described the kind of speculation happening with real estate investors following this method.

Linda McKissack from Texas was drowning in $600,000 of debt, before she invested in 108 rental properties and became a millionaire landlord. Sterling White from Indiana was collecting welfare and selling Pokémon cards until he accrued a portfolio of 400 rental properties in less than four years. Stephanie Betters, a nurse practitioner from North Carolina, manages 1,000 units between shifts at the hospital.

– The Real Estate Evangelist, Financial Times

Say what you will, this sounds insane to me. How are they getting loans to build 1000 unit portfolios as a sidehustle ? Or after “drowning in $600k of debt” ? There’s no way they are not leveraged above and beyond what anyone might consider a safe level. It is reminiscent of the story in the Big Short of the stripper with five home equity loans or the nanny with five rentals. Reminiscent, but on a whole new scale.

As the FT goes on to describe,

Some of the advice doled out by BiggerPockets is not for the faint of heart… Taking out a HELOC (Home Equity Line of Credit), refinancing your home to borrow cash to buy more homes, and taking hard money loans — which are secured by property — at high interest rates to flip houses is risky even when the market is booming.

So yes, very small time investors are getting very risky loans to engage in real estate speculation, at a scale not seen before.

The second type of people who ended up with a bad loan were simply “unsophisticated buyers”, who didn’t understand what they were getting into. And again, we absolutely see this again. Buyers with extremely high PITI, that on a fair recalculation of debt, expenses and income are shooting into the 50-70% DTI range. Sure, on paper, perhaps they fit within the 45% but, in reality, they are in a much more risky position than it appears and they don’t seem to understand that.

The truth is incentives drive behavior and lenders’ incentives are lined up with selling loans, the more the better, the bigger the better. I didn’t understand all the machinations in the Big Short, but I understood one thing, that lenders and the financial markets they sold to, went to extremely creative lengths to sell more and more people risky loans so they could profit off them.

Even if the type of loans are not the same today, I absolutely believe they are bringing the same levels of creativity to the table today.

4. Lenders dropped lending standards

This is essentially the same as the previous, but let’s dive in anyway

Lenders allowed lending standards to become so lax that anyone with a pulse could get a half million dollar loan – whether they could afford it or not… How does a 21 yr old kid get $2.2 million in loans? By EVERYONE looking the other way. The amount of fraud and collusion is unbelievable.

21 year old? Lame. So 2006. Now we have 19 years olds with 45 deals!

Do we really think that lenders back then didn’t know they were making really risky, bad loans ? Of course not. They knew, they found a way to fudge the numbers and stretch the limits, because it’s no risk to them as long as they can turn around and sell that loan to someone else.

Read more: Buyers regretting their monthly payments

Who selects the loan for the buyer and tells them how much they can afford? The lender. And we’d be stupid to assume they are not doing similar things, just because the word “subprime” has disappeared from the lexicon.

More to come

Okay, the author has a few more points but I’ll have to cover those in a later post as this one is quite long already. I’ll leave you with this quote from the Big Short, on the origins of BRRRR.

The baby nurse he’d hired back in 2003 … phoned him. “She was this lovely woman from Jamaica,” he says. “She says she and her sister own six townhouses in Queens. I said, ‘Corinne, how did that happen?'” It happened because after they bought the first one, and its value rose, the lenders came and suggested they refinance and take out $250,000–which they used to buy another. Then the price of that one rose, too, and they repeated the experiment. “By the time they were done they

– Michael Lewis, The Big Short

owned five of them, the market was falling, and they couldn’t make any of the

payments.”

Sounds familiar to me. Next post in this 2 part series is here. This time, its (a little) different.