It’s been a while, life got in the way and Redfin’s unpredictable updates threw my schedule off. Anyway I really wanted to get one in to capture the spring season. Because it has been unexpectedly hot, and definitely a source for concern for us first time homebuyers.

Sellers are holding out more than buyers are holding out.

It’s a fairly hot spring market in San Diego

All Altos Research data is from the San Diego-Carlsbad-San Marcos metro area.

Redfin data is from the San Diego metro on Redfin data center.

Some updates possible if I see updates from these sources.

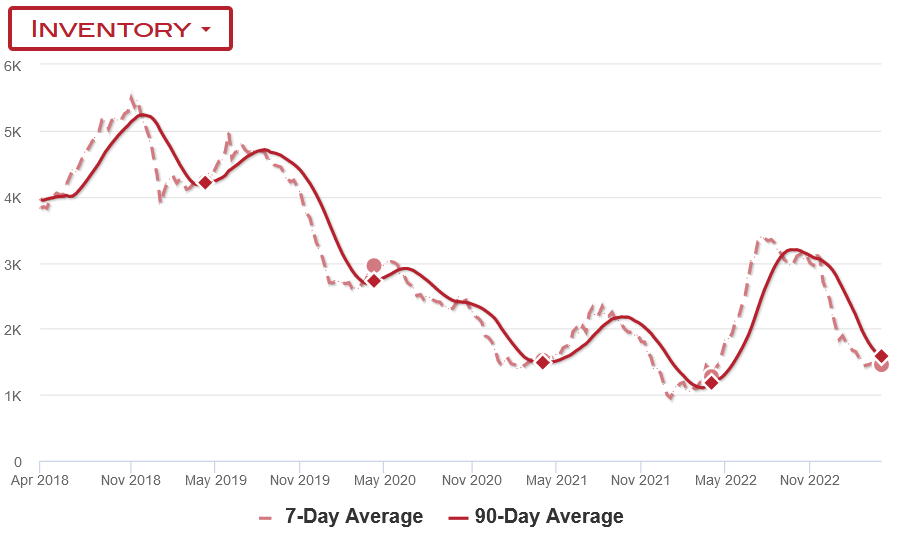

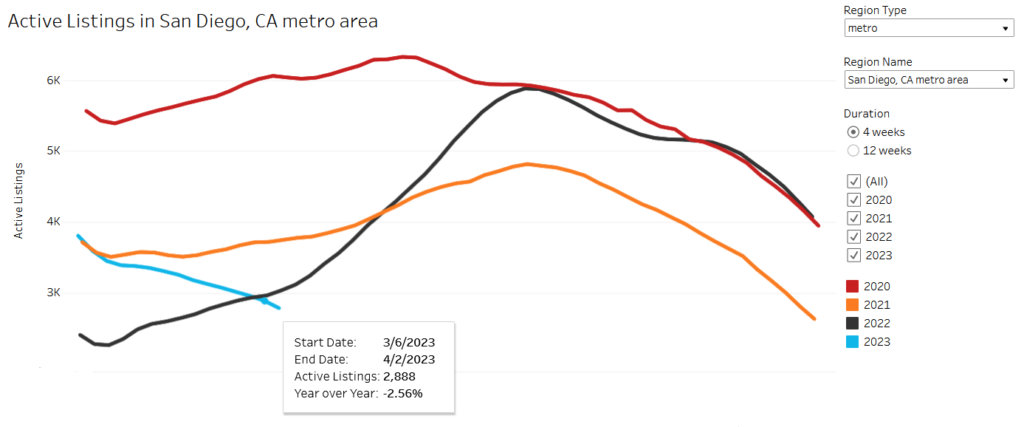

Inventory

Inventory is the main story. According to Altos, it’s almost at the same level as last year. This is pretty depressing given that we had built up quite a bit of inventory last year and it has all been wiped out.

According to Redfin, we’re actually down on inventory compared to last year. And only dropping.

So why is this, when it’s clear the housing market has been hammered and very few sales are happening? Hell, mortgage apps recorded the lowest level since 1995 as recently as late February. Well, as we’ll see this has a lot to do with sellers holding back on listings.

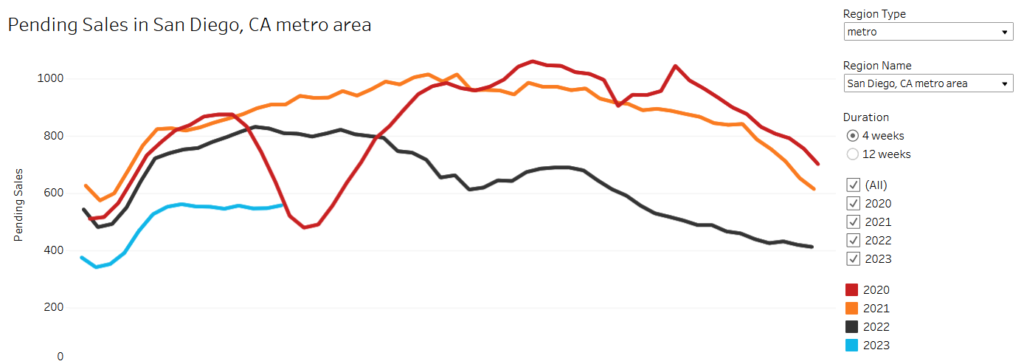

Pending Sales

First let’s look at pending sales. They’re down about 31% year over year. That is quite a drop, basically one out of 3 buyers is not buying this year. It’s a lot worse than even early 2020, pre-pandemic.

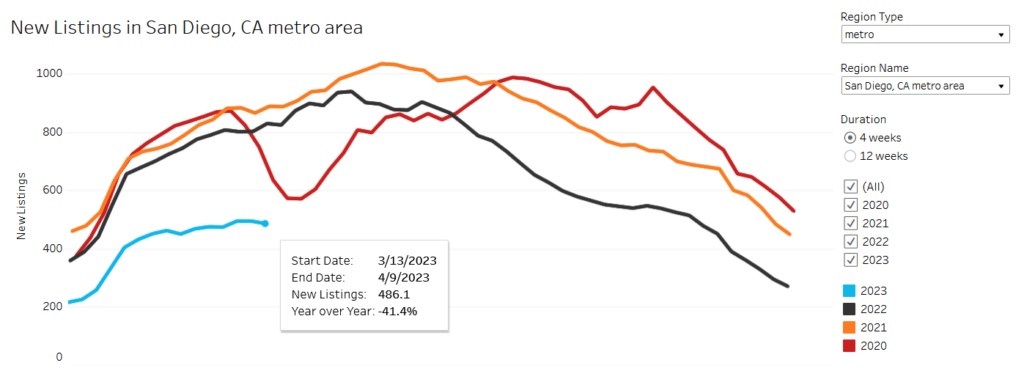

But now let’s look at new listings, because that’s where the problem’s at.

New listings are down even more than pending sales! They are down 41%. So one way to look at it is, the sellers are holding off more than the buyers.

I get that most owner-occupiers won’t give up their low rate to buy another house and pay a lot more. But investors are looking at an increasing rental vacancy rate and looming enforcement of airbnb regulations. That’s in 2 weeks.

All listings specifically for hosting platforms will be removed after the May 1 implementation date if you continue to operate without a license,” Wood said.

– Matt Wood, STRO Program Manager, with the San Diego Office of the City Treasurer.

And while that happens, T-bills are returning 4.5-5% risk free. Anyway, it is after all the hottest season for housing in the year so we’ll see what happens after the season ends.

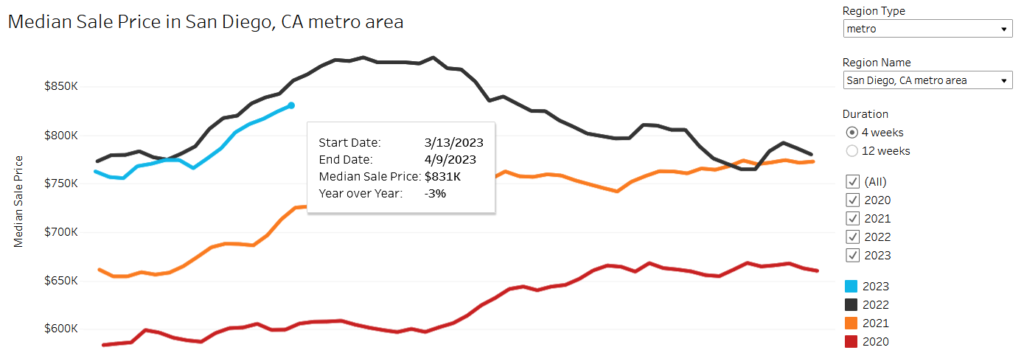

Home Prices

So due to this imbalance of buyers and sellers, prices are rising at roughly the same rate as a year ago, but stay about 2-3% below last year.

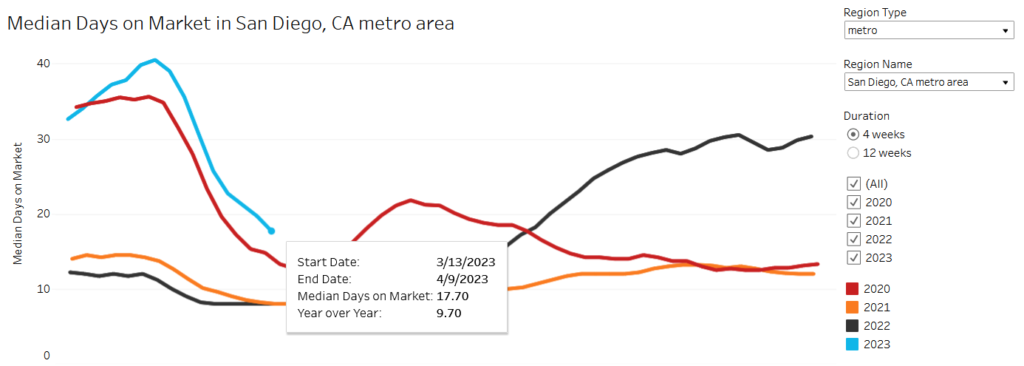

Median Days on Market

One final stat I like to look at is median days on market, which tends to give a sense of how quickly homes are flying off shelves.

This is now at 17.7 which is about 10 days longer than the previous year, and still longer than 2020. But certainly hotter than we’d want to see it with rates at 6.5%

Final Words

What can I say, depressing? Confusing?

I mean, banks are failing, CRE appears to be in dire straits, and … housing is booming? Well at least every time the rates drop a little bit, it seems the demand increases.

In a way the weakening economy is helping housing. How? Lemme explain what I’m seeing. It’s such a weird phenomenon.

The expectation of recession and worsening financial signals is leading investors to seek safety. They do this by buying treasuries and thus lowering 10y rates. Mortgage rates are loosely tied to 10y treasury rates, so this results in lower mortgage rates, which causes a flood of excited homebuyer demand.

To condense that whole paragraph, the expectation of recession and worsening financial signals… causes a flood of excited homebuyer demand. It’s hard to wrap my head around.

So the thing that I’m focusing on instead is, have things gotten better in the general economic picture to suggest a real “return to normal”?

I don’t think so, rates are still high, fed is still committed and predicting a recession, they haven’t pivoted, inflation is still high, yield curve is still messed up, layoffs have increased if anything, regular banks are now failing compared to just crypto last year.

So it seems hard to believe that housing is out of the woods. Even if it is currently experiencing a seasonal boost. Fingers crossed.

Disclaimer: I’m an idiot first time home buyer. I’ve never taken an econ class in my life. I’m just sharing what I see and learn as it happens. I am 100% certain I will get things wrong, so don’t take any of this as the golden truth.

Banks are only failing due to a failure to hedge duration risk on treasuries. They gambled a bit and never fire drilled for such a rapid rate rise. I think it’s the fastest in history and enterprise poorly plans for tail risk. Who would have thought vanilla treasuries would be the downfall of many a financial institution 5 years ago? Layoffs seem to be clustered around companies with B2B exposure as corporations are looking to cut costs while maintaining inflated prices on goods to boost short term earnings metrics. Those with less B2B exposure seem to be reporting flat or increasing earnings. All this to say that while everything on paper seems utterly f’d we apparently shouldn’t underestimate the shear volume of money that poured into the economy during the pandemic that may prop these assets up for year to come. We may see something break if the fed holds rates above 5% and you may get your buying opportunity if it causes some sort of black swan, but it also seems that the fed may pussy out —pivot too soon, drop rates and send housing soaring back to the moon. If only we had a crystal ball we both would be retired.

I agree, it’s a difficult decision to make. Right now it still feels like we are not out of the woods in terms of a serious recession and/or home price correction. So we are piling money away from the difference between cost to buy and cost to rent. If we really get out of this phase with a mild recession, no home price correction, we will just plow that money into extra payments after we buy, reducing the interest and the length of the loan. The danger is as you say, if the fed pivots too soon and housing soars again.

Great data on the website. Q: Are you tracking this bubble in expectation of a crash so you can buy a home?