Today the Fed laid out a plan to unwind its balance sheet. It’s a lot of complex stuff involving caps and redemptions that I don’t totally understand.

But there are a few things I’ve come to understand.

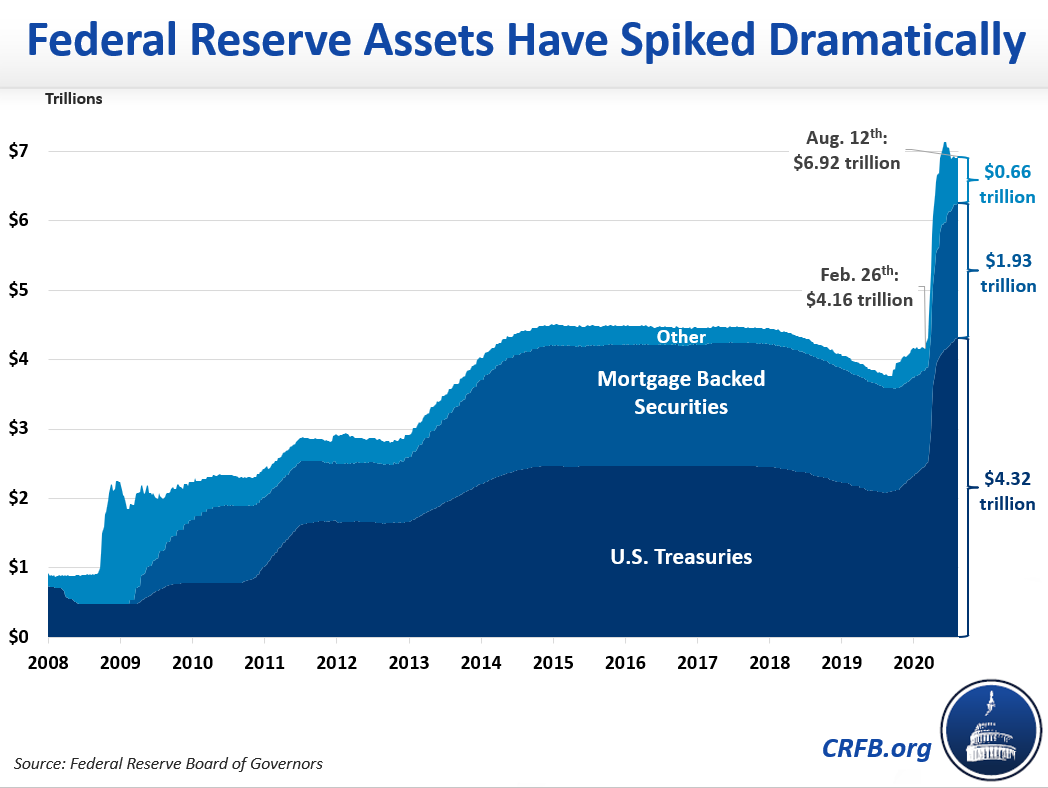

Fed pours trillions into the economy

The first is that starting in 2008 after the financial crisis, the Fed started to buy long-term securities from the market. This is called Quantitative Easing and has the effect of increasing the money supply in the economy and encouraging lending. It basically adds new money to the economy. The benefit is supposed to be that they can then unwind that juice by selling back those securities once the economy is in a stronger position.

Since then, believe it or not, despite the incredible bull run we have experienced for the last 14 years, they have not been able to actually wind that back down to zero. In fact, in 2020, when the pandemic hit, they actually increased the balance sheet rapidly.

You can see here the trillions they have built up since then.

What does this have to do with home prices?

Well, one of the forms of securities that the Fed bought was mortgage-backed securities. As best I can understand, when you get a mortgage loan from a lender, the lender sells the mortgage to the banks, which then bundle them into securities for investors to invest in.

A bank can grant mortgages to its customers and then sell them at a discount for inclusion in an MBS. The bank records the sale as a plus on its balance sheet and loses nothing if the homebuyer defaults sometime down the road.

– Investopedia

So now, the Fed is one such investor for MBS. A very, very deep-pocketed investor.

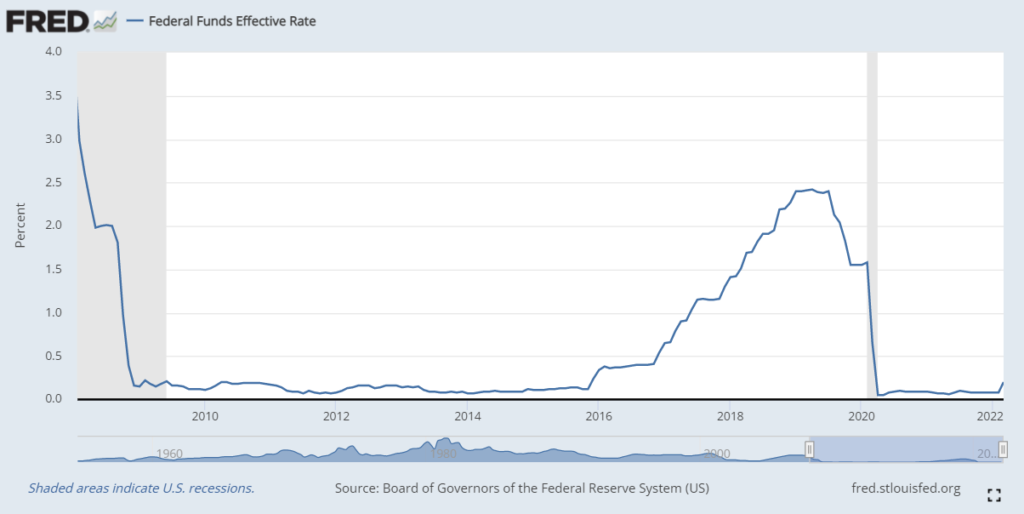

You can imagine, if the banks and lenders know they can sell all these mortgages to the Fed, that’s a lot of incentive to give mortgage loans to people. In a way, this basically provided free money for houses to slosh around the economy. Is it really free? No, it’s a loan, but the Fed also controls the rate at which the money is borrowed. Which they dropped to zero in 2020, so mortgage rates dropped to a stunning low of 2.75% as a result. Very close to free money.

Imagine the government says they’ll temporarily give really cheap loans to anybody to be spent on bags of rice. What happens? Does everybody buy their one bag of rice and go home happy? No, people go on a crazy rice buying spree. They buy multiples and hoard them! The rice sellers capitalize on that and raise the price of bags of rice. Any price goes!

Then other people go to the grocery store and see the empty rice shelves and panic. They also buy bags of rice they don’t need right now in case they’ll be priced out of rice forever! Everyone laments the massive rice shortage. Surely it’s the millennials, the largest rice-eating demographic, hitting prime age.

It’s the Covid toilet paper panic all over again, but with rice, but really with real estate.

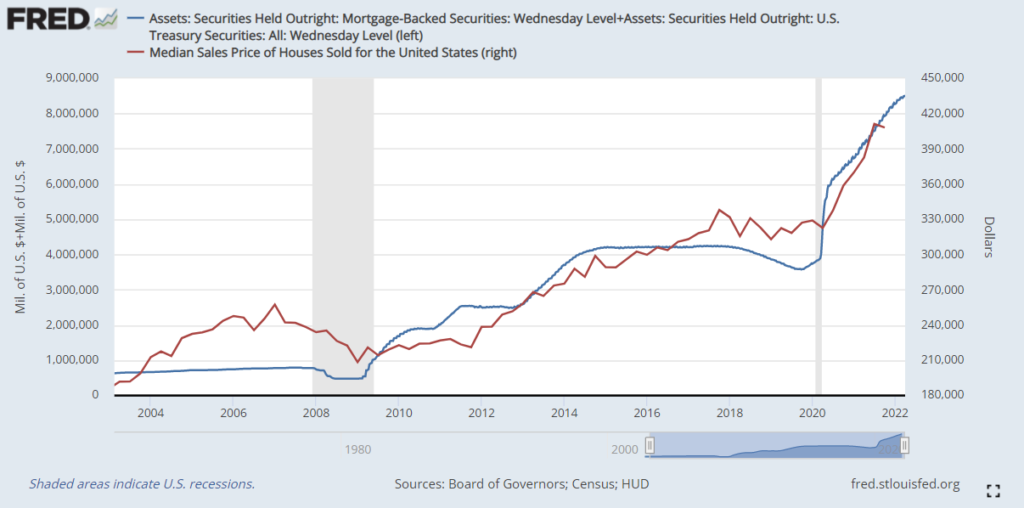

The Fed vs. Median House Price

So Fed buys securities, including MBS, adding trillions of money to the economy, house prices go up. It’s simplistic but in broad strokes, it makes sense. The Fed incentivized the housing market.

Now, with approximately $2.2 trillion of MBS in U.S. federal holdings, economists and strategists are asking whether the Fed is doing more harm than good for a real estate sector in a buying frenzy.

– SPGlobal

“The Federal Reserve’s asset purchases artificially lower interest rates and financing costs, which reinforces the buyer’s need to pay higher prices. It is even further detrimental because the higher price means that the buyer is borrowing more and taking on additional leverage,” said Michael O’Rourke, chief market strategist at JonesTrading, in an interview.

And here’s a gut check. This is a graph of the Fed’s MBS and treasuries (blue line) plotted against the median house prices (red line).

What does the Fed think about all this? Well, mostly that it’s everyone else’s fault, but even they started to worry in 2021.

Some Fed officials see cause for concern. The mortgage-backed securities acquisitions could be having “some unintended consequences and side effects” that should be weighed against their benefits, Robert Kaplan, president of the Federal Reserve Bank of Dallas said on CNBC late last month.

Kaplan isn’t alone in his worry. The home-loan market “probably doesn’t need as much support” as sales soar and prices spiral higher, Eric Rosengren, president of the Federal Reserve Bank of Boston, said during a May 5 virtual event.

– businessinsider.com

So where does it all end? When the Fed stops printing free money for rice. Sorry, real estate. And they did. On March 9th 2022, the Fed ended its QE. However, this just means it stopped buying. It has not sold yet.

This time it’s different

Since I brought up MBS, I really should mention the financial crisis.

Mortgage-backed securities played a central role in the financial crisis that began in 2007 and went on to wipe out trillions of dollars in wealth, bring down Lehman Brothers, and roil the world financial markets.

– Investopedia

In retrospect, it seems inevitable that the rapid increase in home prices and the growing demand for MBS would encourage banks to lower their lending standards and drive consumers to jump into the market at any cost.

That last sentence is funny to me. It’s saying that it’s inevitable that a rapid increase in home prices (which we have) and a growing demand for MBS (which the Fed provided by buying up trillions) would encourage banks to lower their lending standards and drive consumers to jump into the market.

It seems inevitable to me as well. But everyone says, “This time it’s different, this time the buyers are highly qualified!” The average FICO score is this high and the average DTI is this low and everyone is really really behaving themselves.

Okay, but I also don’t trust the financial system to not find a loophole. These are just silly regulations the smartest young minds in our country are paid excessive amounts to find their way around. If you read The Big Short, you get a sense of exactly how creative they were in finding and packaging up those bad loans into highly rated MBS.

But this is a tangent. Back to the Fed and the MBS balance sheet.

Fed has a plan

Finally, today the Fed unveiled their plan to start running off and then selling their treasuries and MBS. Inflation is at an all time high and they need to stop it in its tracks. How fast they do it remains to be seen. For one, they don’t intend to start until May so we’ll have to see.

But for me, the takeaway is that the entire housing market is about to experience a sea change as the Fed sucks all that money right back out of the economy. And it doesn’t seem like a good time to jump in and lock in a lovely, fixed monthly all-time-high and unaffordable house payment.

Only when the tide goes out do you discover who’s been swimming naked.

Warren Buffett

Disclaimer: I’m an idiot first time home buyer. I’ve never taken an econ class in my life. I’m just sharing what I see and learn as it happens. I am 100% certain I will get things wrong, so don’t take any of this as the golden truth.

Thanks for this post — this is an accessible writeup about how some fed policy has reaches into things we can see and interact with in something like the real estate market.

Thanks! Glad it was helpful.