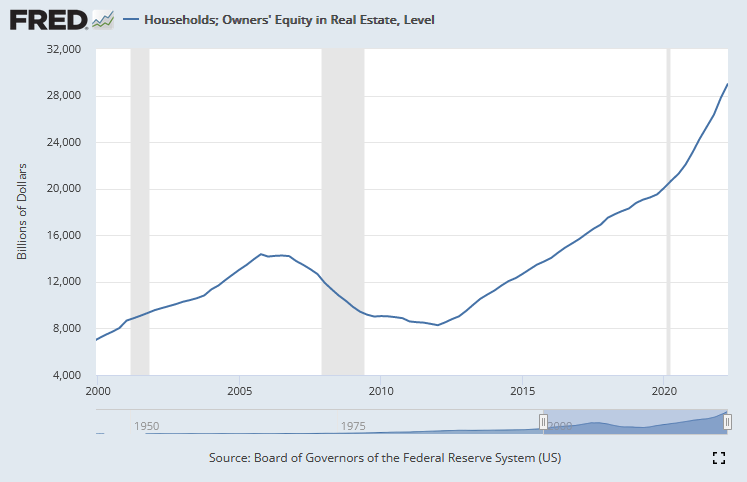

I keep seeing the sentiment repeated that homeowners are in a good position this time to weather a downturn because US home equity is at record highs. This makes no sense to me because it’s like saying beanie babies can’t crash because beanie baby owners have so much sweet beanie baby equity.

Sure, yes, that looks real high. But after 2 years of record appreciation, high homeowner equity means nothing. Of course it’s high, all the appreciation we’ve seen in the housing market went straight to equity. That’s how it works.

If we have a correction, it will come plummeting down as fast as it went up.

Now just to be clear, the higher a single homeowners equity is in their home, the less likely they are to be underwater, so it does protect them. But generally speaking high total homeowner equity is just reflective of and dependent on the bubble we are in.

Leverage inflates equity

In fact, the more leverage there is in the system, the faster “equity” appears to grow. This is because the loan part of equation is fixed, so all appreciation goes into the equity bucket. The less equity a homeowner had to begin with, the faster it grows.

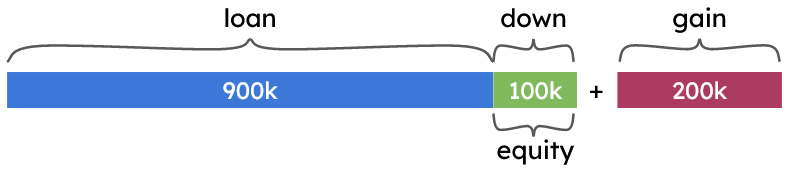

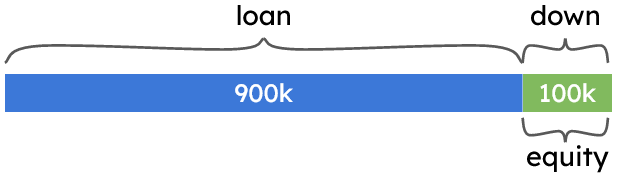

Imagine a person buys a $1m home with 10% down. This means that their loan is for $900k and their downpayment is $100k. They have an LTV (loan-to-value) of 90%, that is, $900k/$1m.

Then the house appreciates 20%, that’s a gain of $200k.

Does this gain get split between the loan and equity? Nope, of course not, it goes straight to equity. Tripling the equity to 300k.

Wow, with just a 20% appreciation in the home, this homeowner’s equity actually tripled! What is this magic!? It’s One Weird Trick! It’s leverage.

Even their LTV looks better – it’s now $900k/$1.2m = 75% LTV.

Notably, if the homeowner had put down 20% (or 200k), his equity would only have doubled. By putting down only 10%, he had more leverage, so his equity multiplied faster.

Zooming out

The same thing plays out on the national level. To simplify, let’s say US homeowners have 100m in equity in total and all houses are $1m each.

If each homeowner has 10% equity that means each homeowner has $100k in equity. And therefore that 100m national homeowner equity represents 1000 mortgages.

$100,000 equity * 1000 mortgages = $100M homeowner equity

If there is a 20% rise in home prices – making all houses worth $1.2m, then each homeowner now has $200k more equity, as in the example above.

$300,000 equity * 1000 mortgages = $300M homeowner equity

Wow! Again triple the equity for a 20% appreciation in price. And that’s why equity skyrocketed since the pandemic. Because appreciation goes straight to equity and leverage has a multiplier effect. Not because homeowners were putting down larger downpayments.

Just to be clear, it’s not that all homeowners have 10% equity. That was just for illustration purposes.

Depending on the age of the loan it varies and the national average LTV is currently 42% across all mortgages. So some people, especially those who bought prior to 2020 and did not do a cashout refinance, are definitely in safe territory with high LTV.

But this example illustrates how that leverage affects the part of the market who put 10% down very recently.

Why does it matter?

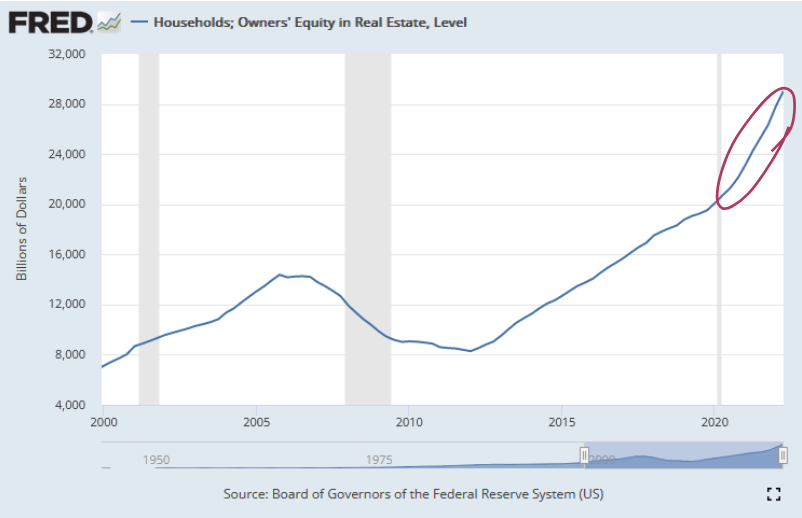

Okay, you might be saying, why does it matter how they got high equity? Now that they’re there, aren’t they in a better position to weather a downturn? Not at all. Because it deflates at the same rate.

In the example above, if the home goes back to $1m (which is less than 20% down actually) then the equity goes back down to $100k. Bye bye, magic. 20% decline in price –> 1/3 the equity.

So when people say the housing market can’t crash because homeowner equity is so high, it’s nonsense.

Here’s a quote:

Home equity is at the highest it’s ever been, and it is continuing to increase at rates we have never seen before. This is allaying fears of another housing crash, as homeowners are less likely to be upside down in their homes should prices drop steeply (which, as we’ve mentioned before, is very unlikely).

– Neo Home Loans

Not true, it will come down as fast as it went up. The high LTV loans especially inflate equity and then deflate just as dramatically.

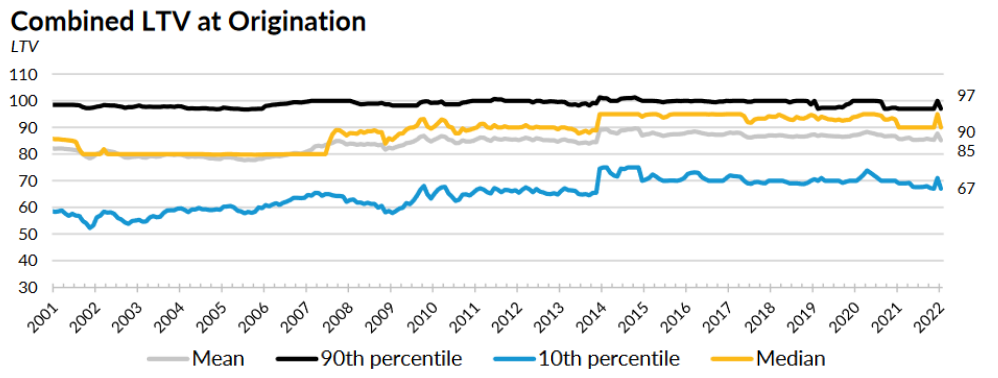

Median LTV

You might be wondering though, if average LTV is 42% then that would take a mega crash greater than 58% to wipe out that equity. Yes, and that’s unlikely but again, that’s an average of mortgages going back many years.

Let’s look at the mortgages originated in the last 2 years.

The median LTV for owner-occupied (OO) purchases during the pandemic was 90%. So if you were to put all pandemic homebuyers into buckets according to equity at the time they got the loan, 50% of them would end up in the same bucket. They all got their loan with 10% or less equity.

Which means 50% of pandemic OO buyers will be underwater if the correction wipes out 10% of their purchase price. That’s a big yikes.

But… not in San Diego, right?

Sounds too doomer-y? This can’t happen in our lovely San Diego, right?

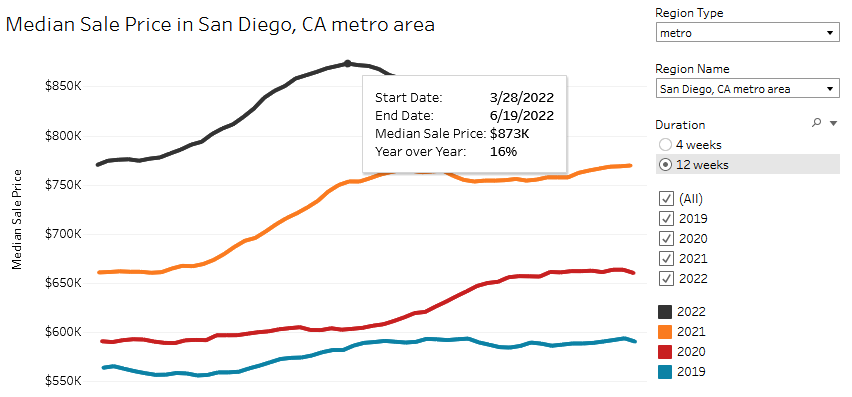

Let’s take the median purchase at the peak this year in San Diego, let’s take the 12 weeks the market was hottest. Redfin lets us find the median of the 12 weeks from April through mid June – it’s 873k.

Half of all buyers put 10% down so that would be $87k. That was their equity at the time of purchase.

They probably haven’t made much of dent in the loan yet.

So they would be underwater once their home price drops to 873k – 87k = 786k.

Guess what the latest data from SDAR (San Diego Association of Realtors) says median home price in San Diego is this week. 780k.

That’s right, buyers who bought at the peak this spring in San Diego are likely already underwater. The correction has barely gotten started. And that’s why “record home equity” doesn’t really mean shite.

One last thing – being underwater sucks but it doesn’t mean those buyers lose their home or get into any trouble. If they can continue to pay their mortgage and stay in the house, they’ll be fine. But if for some reason they can’t, their options become very limited and foreclosure becomes more likely.

The main point is that “high homeowner equity” isn’t protection against a correction or crash in a bubble, because it’s inflated by said bubble. Fixed rates are protective, low DTI is protective, stable jobs are protective. High homeowner equity is paper money and can evaporate as quickly as it appeared.

Disclaimer: I’m an idiot first time home buyer. I’ve never taken an econ class in my life. I’m just sharing what I see and learn as it happens. I am 100% certain I will get things wrong, so don’t take any of this as the golden truth.