Mortgage rates have been the biggest story of this month. Earlier this year, many believed that rates would not go above 4% in 2022. Hell, I thought they wouldn’t go above 6.5%. And here we are, at the end of the October having 7%+ mortgage rates since Oct 5th.

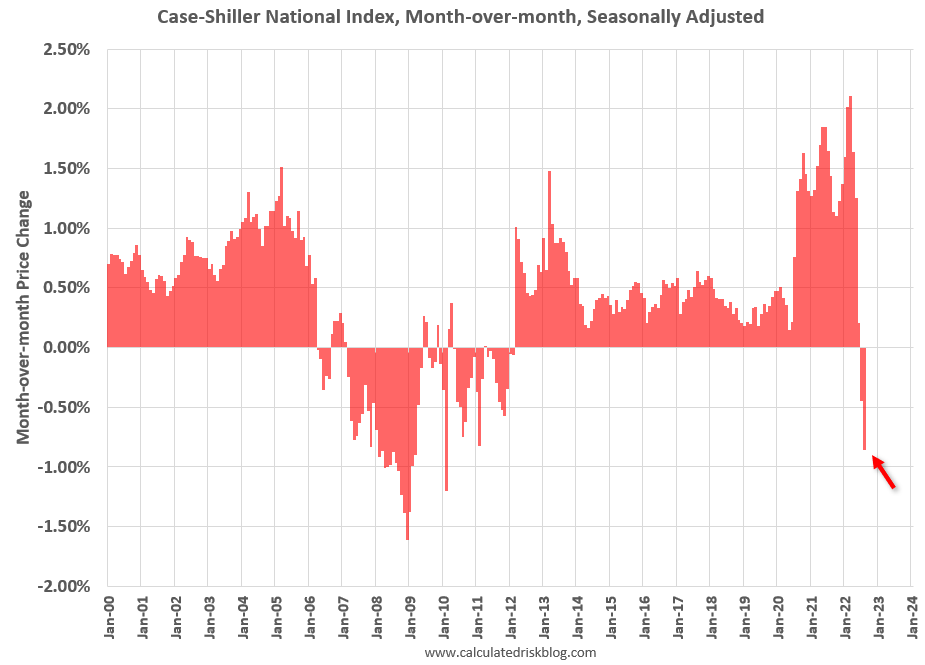

Theme of the month: Okay, if Case-Shiller is twisting our arms, we’ll admit prices are now falling.

The high mortgage rates have pushed homes out of the reach of all but highest paid, and resulted in a chilling effect on the housing market. Mortgage purchase applications are down 90%(!!) from a year prior.

Media

Housing Market Hits Brakes as US Prices Fall Most Since 2009

In October, something momentous happened, which is that the Case-Shiller started to report a drop in home prices. Although this measure is lagging, it is largely unimpeachable, so few can dismiss it. Bloomberg included. They reported the largest month-over-month fall since 2009.

A measure of prices in 20 large US cities in August fell 1.3% on a month-over-month basis, the most since March 2009, according to the S&P CoreLogic Case-Shiller index. That’s the second-straight month of declines.

It’s true this is just saying something we all knew from all the data that is more current. But it’s good to see the Case-Shiller index echoing it.

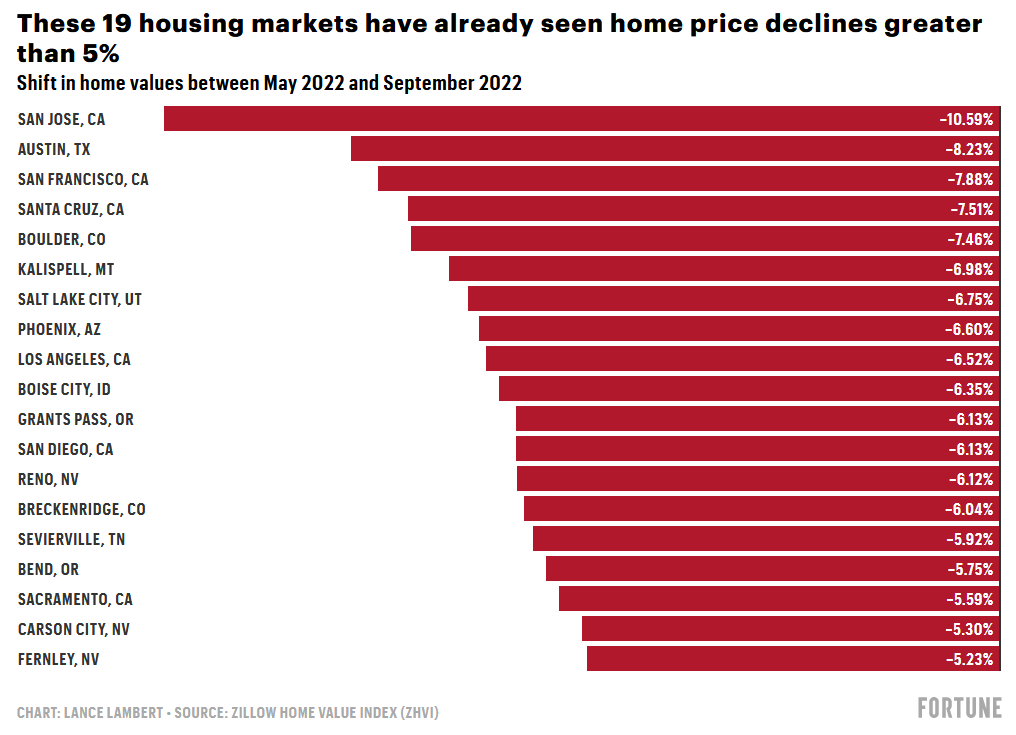

In fact, San Diego was one of the cities shown to have fallen the most…

On a month-over-month basis, cities on the West Coast including San Francisco, Seattle and San Diego fell the most.

We’re already seeing sharp home price declines in many markets

Fortune continues to be the most willing to report the fall in the housing market, mostly through Lance Lambert. I swear to God, this kid will win some accolades for his reporting during this time.

He reports that the 2 sets of markets getting hit the hardest at this time are frothy markets like Boise, Austin and Phoenix, and high cost tech hubs like San Francisco, San Jose and Seattle.

One thing to note though, the markets showing price declines are largely on the west coast. Those on the east coast and florida are still seeing a relatively warm market.

Home Builders Warn Prices Could Tumble Another 20%

Builders are reacting a lot quicker this time . In 2008 they refused to believe that the housing market was falling and they got burned, building too much and investing too much. This time they are pulling back faster, and have been dropping prices and offering incentives.

But, with rates rising, the improvements in demand are short-lived.

Home builder confidence plunged for a tenth straight month in October as rising interest rates continued to weaken housing demand—prompting economists to warn an unexpected rise in new home sales last month may be short-lived and prices may be on the brink of collapse, the National Association of Home Builders reported Tuesday.

RE Industry

Bubble or not, home prices could fall—a lot

Surprisingly level headed article from Realtor.com for once. Goes over why things are different than 2008 – the usual stuff, “nearly all of those bad, subprime loans have been eradicated” and “most homeowners will simply stay put to weather the real estate storm.”

But goes on to say, even “with a stronger housing market, home prices could still fall. A lot.” What a surprise! They were refusing to say as much a few months ago, insisting prices would just plateau. Of course, now that Case-Shiller is already falling, it’s hard to pretend it’s not happening.

Habib, of MBS Highway, expects prices could drop 6% to 7% in these hot markets and dip just 1% to 3% everywhere else.

McBride, of Calculated Risk, expects prices could fall 20% in these areas compared with a 10% decrease nationally.

“If you define a bubble as home prices are starting to fall, then we’re probably in one,” says McBride.

Even McBride was forecasting prices to hold a few months ago, so it’s significant that he’s now forecasting 20% in some markets.

“Renting is 100% interest”

This garbage take is gaining much popularity with the realtor’s these days. Who of course think it’s always a good time to buy.

There are deals out there, says Brikelle Corcoran, a realtor who works with active military buyers and sellers in Yuma, Arizona. “Several of my local lenders have a temporary buy-down program that allows buyers to buy down their rate temporarily by 2%, which lowers their monthly payment, she says.

Still, the alternative for many buyers is renting, and as Corcoran notes, ” the interest rate on rent payment is ALWAYS 100%.”

It’s nonsense of course, because they are trying to make you compare the prevailing 7% rate with 100% but that’s not really how that works. Sure, rent doesn’t build equity you are paying for shelter and that’s ok. More people would be surprised to look at how much they are throwing away on interest in their monthly payment, while they believe it’s all going to equity.

Anecdata

“I bought a house recently and haven’t even made my first payment yet.. as excited I was to buy the house it made a complete 180. I am 24 years old and a veteran … as much as I love the idea of being a homeowner I don’t think I can live here anymore and it’s driving me insane” – Young homebuyer bought a home in the boonies with no apparent need, just because they loved the idea of being a homeowner.

“When we are ready to close, if we are seeing our exact same house sold for $40k less than what we are contracted to, what does that mean for us?” – Homebuyer who got into contract with builders finding that newer houses are listing for less. This is a common situation, can’t imagine why buyers jump on price dropping builds, only to be upset about the continuing drops.

“Without a lender, without any recourse, and most importantly, without a home, I am forced to end my homebuying adventure and back out of the contract. The builder is claiming “pandemic delays”, which allows them to unilaterally extend the closing date without recourse.” – Another homebuyer losing due to builder delays. Buyers, beware new incomplete builds, too much risk to carry in uncertain times.

“I sold my house and lost about 100k equity and 150k in upgrades, and I couldn’t be happier. I sold a money pit of a flip very recently. I was depressed, anxious, and angry for over two years, trying to get it done … so I could “flip it” before a crash came. Because even I knew home prices were too dang high at the time.” – Flipper glad to offload a property at a loss.

“Just underachieving people hoping the world crumbles so everyone can be as miserable as they are. I’ve never heard r/ReBubble summed up so accurately.” – Homeowner scoffing at a reddit sub that has been sharing data and warning about a potential crash for a year.

“I’ve seen a few theories spread on r/REBubble (i.e. widening spread between 10/y and mortgage rates) actually come to fruition. A lot of noise, but still some gems” – Lance Lambert, Fortune reporter who has been covering the correction, shouting out the same sub.

Disclaimer: I’m an idiot first time home buyer. I’ve never taken an econ class in my life. I’m just sharing what I see and learn as it happens. I am 100% certain I will get things wrong, so don’t take any of this as the golden truth.