Want to see one of my favorite listings that illustrates everything that is wrong with this market?

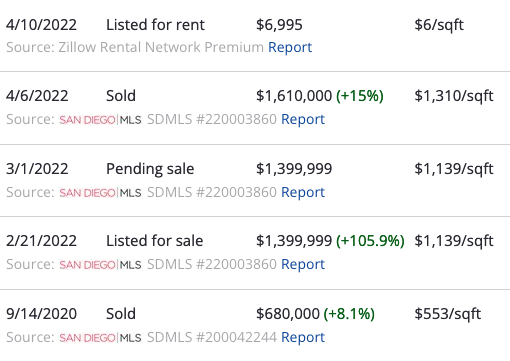

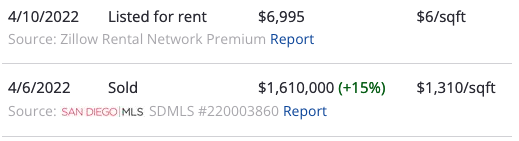

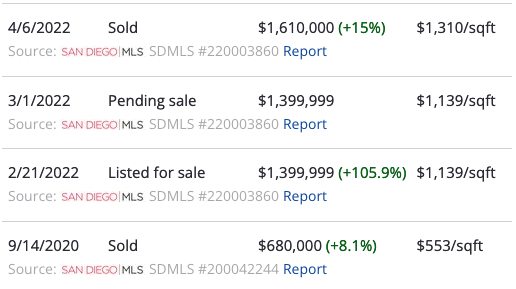

In early April, a house popped up to rent in my area. I’m not looking to rent but I’ve been watching the rental market for softening. This house is a 4/2 in a quiet neighborhood in San Diego. But It had been sold just four days prior at $1.6m and then listed for rent at $7000.

Does a tech bro want a house in a quiet, unwalkable area overlooking the freeway? I mean, I know tech bros and the answer is no.

It’s a nice enough house as you can see and even has a mini-ADU. It’s clearly been recently renovated, of course with plenty of grey LVP and white paint. Here’s the listing on Zillow.

What’s wrong with this picture?

So what’s not to like? Well, here’s the history on this place until they listed it… let’s talk through what’s wrong with this picture.

Asking rent

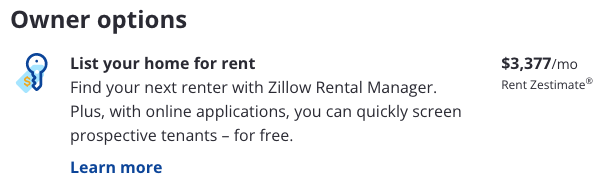

So the owner buys the house and immediately lists it to rent for $7,000. That in itself is crazy. This house is in an area which is currently renting for $3-4k. Right now, at what might be the peak of the housing bubble, when rents have skyrocketed, even Zillow lists the rent estimate at $3,377.

So why on earth do they think they can get $7000 for it? Who rents a normal home for $7000? Are they expecting some sort of tech bro to be this stupid?

Come on, the tech bro would just buy a house if they were that baller. And this isn’t even a baller house. I mean, it’s nice, but it’s deep in the neighborhood, unwalkable to the main street area that makes this area desirable, and bang on top of the freeway.

Does a tech bro want a house in a quiet, unwalkable area overlooking the freeway? I mean, I know tech bros and the answer is no.

Cash flow

This house probably costs more than $8000 a month on the mortgage, and they listed for $7000.

So right off the bat they were intending to rent it out for less that the mortgage? Even if they bought it with cash, you really want to make a good “cap rate”, back of the envelope math suggests you

- Take prevailing rent for the year: $44,400

- Subtract 10% for property management: ~$40,000

- Then divide by what you paid ($1.6m) to get: 2.5%

They locked up $1.6m for a measly 2.5%? I don’t understand.

Appreciation

Alright, so maybe they are counting on appreciation – did they get it undervalued? Maybe they were hoping it would go up in price over the next year. This is called speculation by the way.

The place listed at $1.4m and they paid $1.6m so they overbid 200k. And the place previously sold a scant 18 month earlier for $680,000! That’s 235% appreciation already baked in the price.

Now, granted the previous buyer was a flipper who did renovate the property. So that price partially reflects improvements they made but the facts stand. Given such a high level of appreciation over less than 2 years, it’s extremely risky to expect further appreciation when you overpaid by that much.

Results?

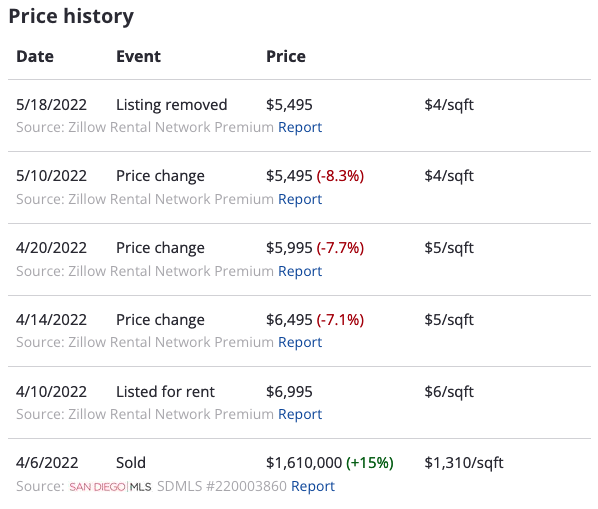

So were they successful? Did they find the unicorn renter who wants to pay $7000 for this place? Let’s see…

Womp womp. They reduced the rent repeatedly over the 2 months and ultimately have unlisted as of this week. Maybe they managed to rent it at $5500.

One of the key risks I see in this bubble is this proliferation of people investing in real estate seemingly with no conception of how to make the numbers work. I don’t even know much about this and yet 2 months ago when this listing popped up, I laughed because it was so obvious that it wouldn’t rent out at $7k.

I suspect that many of these investors have been succeeding in the last 2 years largely because record appreciation was covering up their failures and bad decisions. As the tide turns, we will see more and more of these “investments” failing. My expectation is that these properties will start showing up for sale.

While some investors truly do have deep pockets, I suspect that many are overleveraged and will actually be in a very bad position as the house of cards collapses. Those that used creative financing will find themselves with loans they can’t handle, because while mortgages are heavily regulated and tracked, we have no idea how much risk has been building in this part of the market.

Disclaimer: I’m an idiot first time home buyer. I’ve never taken an econ class in my life. I’m just sharing what I see and learn as it happens. I am 100% certain I will get things wrong, so don’t take any of this as the golden truth.